Income Tax

Introduction

Understanding how taxes work in Switzerland is an essential part of planning your move and managing your finances confidently.

At Swiss Together, we aim to make this complex topic easier to navigate by providing you with an overview of the Swiss income and wealth tax system — specifically for foreign residents.

Please note that this overview is for informational purposes only and does not replace professional tax advice. For a precise assessment of your personal global tax situation, we strongly recommend consulting a qualified tax professional.

The following is a guide that outlines the key elements of the Swiss tax framework — what types of taxes exist, how they’re applied, and what factors can influence your personal tax position — so that you can make informed decisions about your relocation and settlement.

However every individual’s financial situation is unique, we always recommend consulting a qualified tax advisor for personalized advice.

Income Tax

In Switzerland, income tax is levied at four levels of government:

- Federal (national)

- Cantonal

- Municipal

- Church

The total tax rate you pay will depend on your canton and municipality of residence, as each has its own tax regulations and rates.

Church Tax

If you register as Catholic or Protestant, you’ll automatically be subject to a church tax (impôt ecclésiastique / Kirchensteuer / imposta di culto).

Those who register as members of another faith, or as non-religious, are exempt.

Withholding Tax

Foreign nationals who do not hold Swiss citizenship and do not have a permanent (C) residence permit, and who are not married to a Swiss citizen or C-permit holder, are generally taxed through withholding tax (impôt à la source / Quellensteuer / imposta alla fonte).

This tax is automatically deducted from your monthly salary and includes all components — federal, cantonal, municipal, and church.

Most newcomers, who typically receive a B or L permit, are subject to this system.

How your income level matters

Annual income below CHF 120,000:

The withholding tax rate is determined by your canton of residence only (not your municipality).

No additional annual tax return is required.

Annual income above CHF 120,000:

You must submit a tax declaration (Steuererklärung / déclaration d’impôt / dichiarazione fiscale) at the end of the fiscal year.

Your final tax is then recalculated based on your total global income and assets — just as for Swiss citizens or C-permit holders.

In this case, your municipality also affects your final tax burden.

Ordinary Income Tax

Swiss citizens and foreign nationals with a C permit are subject to ordinary income tax. This tax is usually paid once per year, either in one or several instalments.

An estimated tax bill is typically issued early in the fiscal year (around February or March), based on the previous year’s income.

After the year ends, you submit a statutory declaration and the final tax amount is recalculated accordingly.

Wealth Tax

In addition to income tax, Switzerland levies a wealth tax at the cantonal, municipal, and sometimes church level.

There is no federal wealth tax.

Wealth tax applies mainly to individuals with significant assets — typically above CHF 2 million — and is based on net assets (total assets minus debts).

Rates differ by canton and generally range from 0.18% to 0.7%.

Canton of Zurich vs Canton of Schwyz – Tax Comparison Overview

1. Income Tax (Cantonal Level Only)

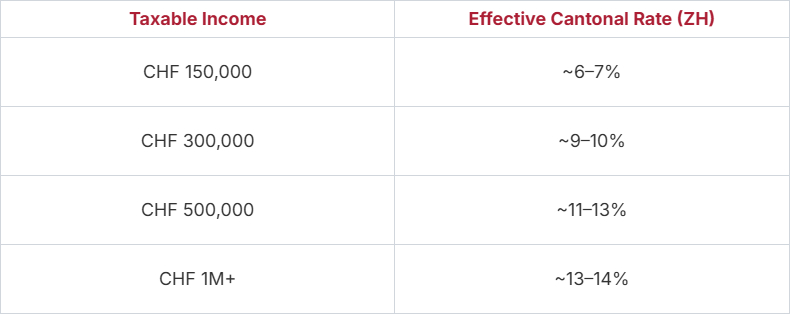

Canton of Zurich (ZH)

- Progressive tax system

- Higher base cantonal tax level

Approximate effective cantonal rates:

Note: The municipal multiplier is applied after the cantonal base tax is calculated.

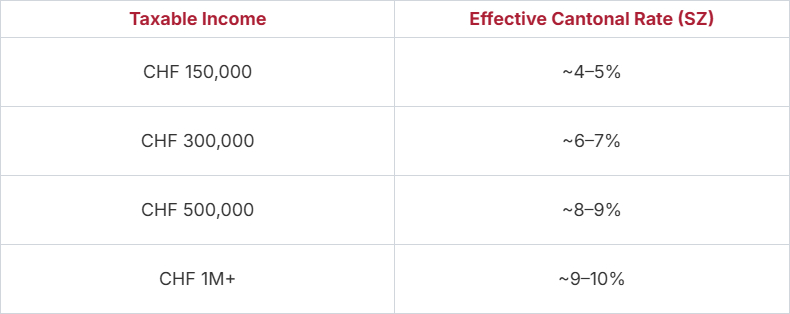

Canton of Schwyz (SZ)

- Progressive tax system

- Significantly lower cantonal base tax level

Approximate effective cantonal rates:

Example: Wollerau municipal multiplier ~65–70%.

Big Picture Difference

At higher income levels, Schwyz total tax burden can be approximately 20–35% lower than Zurich. The difference becomes substantial above CHF 400,000–500,000 taxable income.

This is why municipalities such as Wollerau and Freienbach are particularly attractive for high earners and entrepreneurs.

2. Wealth Tax Comparison

Zurich (ZH)

- Progressive wealth tax

- Effective range typically ~0.15% – 0.30% (before municipal multiplier)

Schwyz (SZ)

- One of the lowest wealth taxes in Switzerland

- Effective range typically ~0.05% – 0.15%

For individuals with CHF 5M–10M+ net assets, this can result in very significant annual differences.

3. High-Level Illustration

Taxable income: CHF 500,000

Net wealth: CHF 5,000,000

Living in Zurich canton → significantly higher total tax burden.

Living in Schwyz (e.g., Wollerau) → potential savings of tens of thousands of CHF per year.

For further calculation examples, please refer to www.comparis.ch.